A few years ago, payday used to follow the exact same pattern every time.

I’d get paid Friday morning, buy groceries Friday afternoon feeling cautiously optimistic, maybe grab takeout that night because things finally felt a little less tight, and then by Monday evening I’d already be opening my banking app trying to figure out where everything went.

The mortgage was coming out Wednesday. The power bill was due Thursday. One kid suddenly needed $17 cash for a school field trip I vaguely remembered signing a form for three weeks earlier. Car insurance was renewing. The internet bill was sitting there waiting. Some subscription I forgot existed quietly charged my account again.

By the following Tuesday night, I’d be standing in the kitchen doing silent math while questioning whether I could afford the cheese I was grating into a casserole.

That was my actual financial life for a long time. Not irresponsible spending. Not shopping sprees. Just too many things pulling from the same account at the same time.

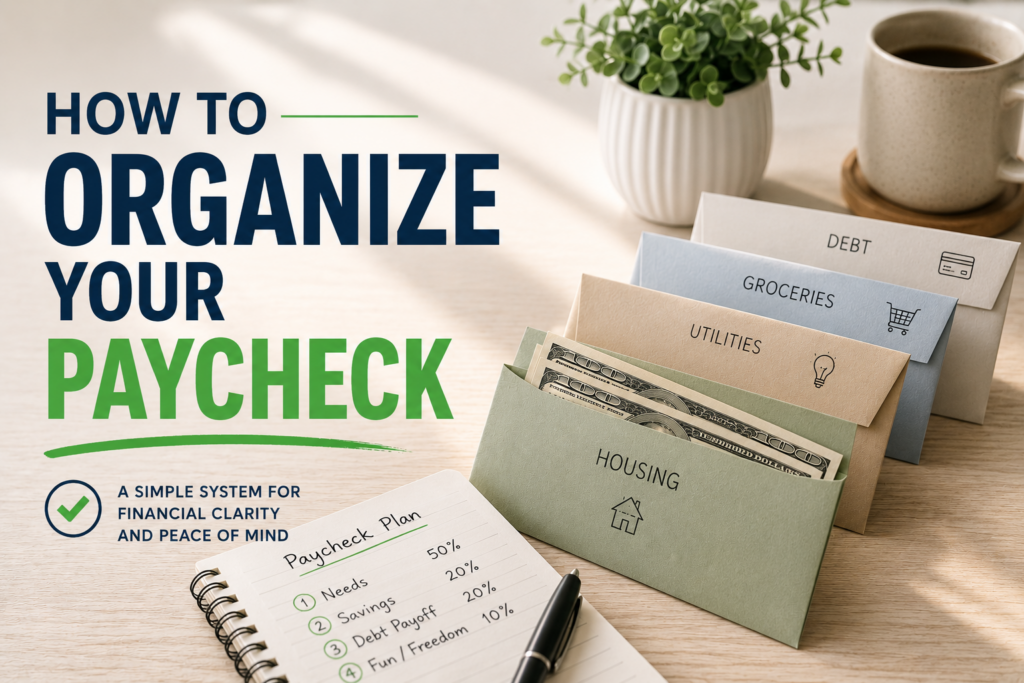

I used to think I needed a stricter budget, but eventually I realized I needed my paycheck organized before spending even started. That’s a huge part of what the Money Lane System focuses on — separating money early so bills, spending, and future goals stop colliding with each other all month long.

Why Everything Felt So Financially Exhausting

For years, every dollar landed in one account. Mortgage money, grocery money, gas money, insurance money, school stuff, subscriptions, life maintenance — all sitting together until none of it felt clear anymore.

So even normal purchases always carried this low-level anxiety underneath them. I’d stand in the grocery store debating which shampoo to buy because somehow every bottle suddenly costs eleven dollars, while also trying to remember whether the equalized power payment had already cleared.

That kind of mental juggling wears people down slowly. Especially when you’re already busy. Especially when money has felt stressful for a long time. Especially when you’ve downloaded budgeting apps before and abandoned them three days later because categorizing drive-thru coffee purchases at 10:47 p.m. felt deeply unnecessary to your survival.

After a while, I realized I wasn’t bad with money. I was tapped out from manually keeping track of everything all the time. I think that’s why so many people eventually start looking for lower-maintenance ways to manage money. The Easiest Money Routine for People Who Hate Budgeting really comes down to reducing the amount of mental energy your finances require every day.

The One Change That Actually Helped

I opened a separate account strictly for bills.

I didn’t build some complicated financial setup. It was literally just one separate account for fixed expenses.

That account became home for the mortgage, equalized utilities, insurance, internet, phone bill, subscriptions, loan payments, daycare, recurring apps, and automatic withdrawals. Every payday, money moved there first automatically before groceries, before spending, before real life had a chance to interfere.

My stress level dropped noticeably because I didn’t have to think about whether I would bounce a bill payment or have enough to cover everything.

Why Automatic Income Splitting Works So Well

People talk about financial organization like it’s entirely about discipline, but a lot of it is visibility.

When fixed expenses are separated from spending money, your brain stops trying to keep a running spreadsheet in the background all day long. You stop wondering whether the money in your account is actually available or already spoken for. You stop mentally subtracting bills while standing in line at the pharmacy. You stop opening your banking app six times a day trying to remember what still needs to come out.

A lot of financial stress comes from uncertainty. When everything sits in one account together, every purchase feels slightly unclear. Grocery money sits beside mortgage money. Gas money sits beside the internet bill. Your brain keeps trying to track all of it manually.

It’s so freaking exhausting.

Separating fixed expenses into their own account creates clarity almost immediately. Suddenly the mortgage payment is already handled. The insurance money is already waiting. The equalized power bill stops sneaking up halfway through the month. And because those expenses are separated first, the money left in your regular account finally feels honest.

If payday still feels stressful no matter how much budgeting you try, What to Do Every Payday Before Your Money Disappears walks through a much simpler paycheck setup that takes about ten minutes.

How to Split Income Automatically Without Making It Complicated

The simplest setup is usually the one people actually stick with.

Start with a bills account and add up your fixed monthly expenses — rent or mortgage, utilities, insurance, subscriptions, loan payments, daycare, recurring bills, and automatic withdrawals. Then divide that number by however often you get paid.

Every payday, automatically transfer that amount into the bills account first.

Now your mortgage money is already waiting where it belongs instead of floating around beside grocery money and a late-night Amazon purchase you barely remember making.

I still kept a separate spending account for groceries, gas, and everyday life maintenance, and eventually added a savings account too. But separating fixed expenses first was the part that changed everything for me.

If you’re trying to organize your finances without tracking every dollar, this works surprisingly well because it removes so much decision-making before spending even starts.

Why Traditional Budgeting Burns People Out

Most budgets require constant attention.

They assume people will consistently track spending, categorize purchases, review numbers, and make careful decisions even when they’re exhausted. But exhausted people usually prioritize convenience because they’re exhausted.

Nobody finishes a brutal Tuesday wanting to update expense categories. They want dinner. They want the kids settled down. They want one thing in life to stop requiring mental effort for five minutes.

That’s why automatic paycheck organization works better for many overwhelmed people than detailed budgeting systems ever did. The less your finances rely on daily willpower, the more stable they usually become.

I eventually realized I wasn’t failing at budgeting. I was mentally drained from constantly managing money manually all the time. That’s also why my posts Why Budgets Don’t Work and How to Organize Your Money Better and Stop Living Paycheck to Paycheck hit such a nerve for people. Most financially overwhelmed people are already mentally overloaded before budgeting even starts.

The Biggest Relief Was Mental

I still had bills. I still had responsibilities. I still had unexpected expenses.

But I stopped feeling financially blindsided all the time.

The mortgage was already covered. The power bill was already sitting there waiting. The internet payment stopped sneaking up on me every month. And because those fixed expenses were separated automatically, the balance in my regular account actually meant something.

For the first time in years, I could look at my spending money without needing a full investigation into what bills were still pending.

The first time I noticed money still sitting in my account from the previous paycheck, I actually reopened my banking app because I thought something was wrong.

That feeling is hard to explain if you’ve lived in constant financial confusion for a long time.

If You’re Overwhelmed Financially, Start Smaller Than You Think

A lot of people delay organizing their finances because they think they need more income, perfect self-control, a complete budget, or a total financial reset.

You probably don’t.

You might just need your fixed expenses separated before life starts spending your paycheck for you.

That one change can create an incredible amount of breathing room mentally. Not because it solves every financial problem overnight, but because clarity reduces panic.

And panic gets expensive fast.

The Goal Isn’t Becoming Perfect With Money

Most people are not trying to become financial experts. They just want money to stop feeling so exhausting. They want groceries without mental math. They want payday to last longer than a weekend. They want to stop wondering whether the account balance is lying to them.

The Free 10-Minute Paycheck Plan is built around this exact idea: decide where money goes immediately when the paycheck arrives instead of trying to organize everything afterward.

Because once all the money mixes together, life usually spends it faster than expected.

And after years of trying to mentally track everything myself, I just couldn’t anymore.

It’s so freaking exhausting.

Now my bills are separated before spending starts, and for the first time in years, I actually still have money sitting in my account from the previous paycheck.

I cannot explain how different life feels now. It’s been life altering.