My husband spent years trying to create something neither of us could quite put into words at the time. We called it financial stability, but what we really wanted was to stop feeling like every unexpected expense had the power to throw us off course.

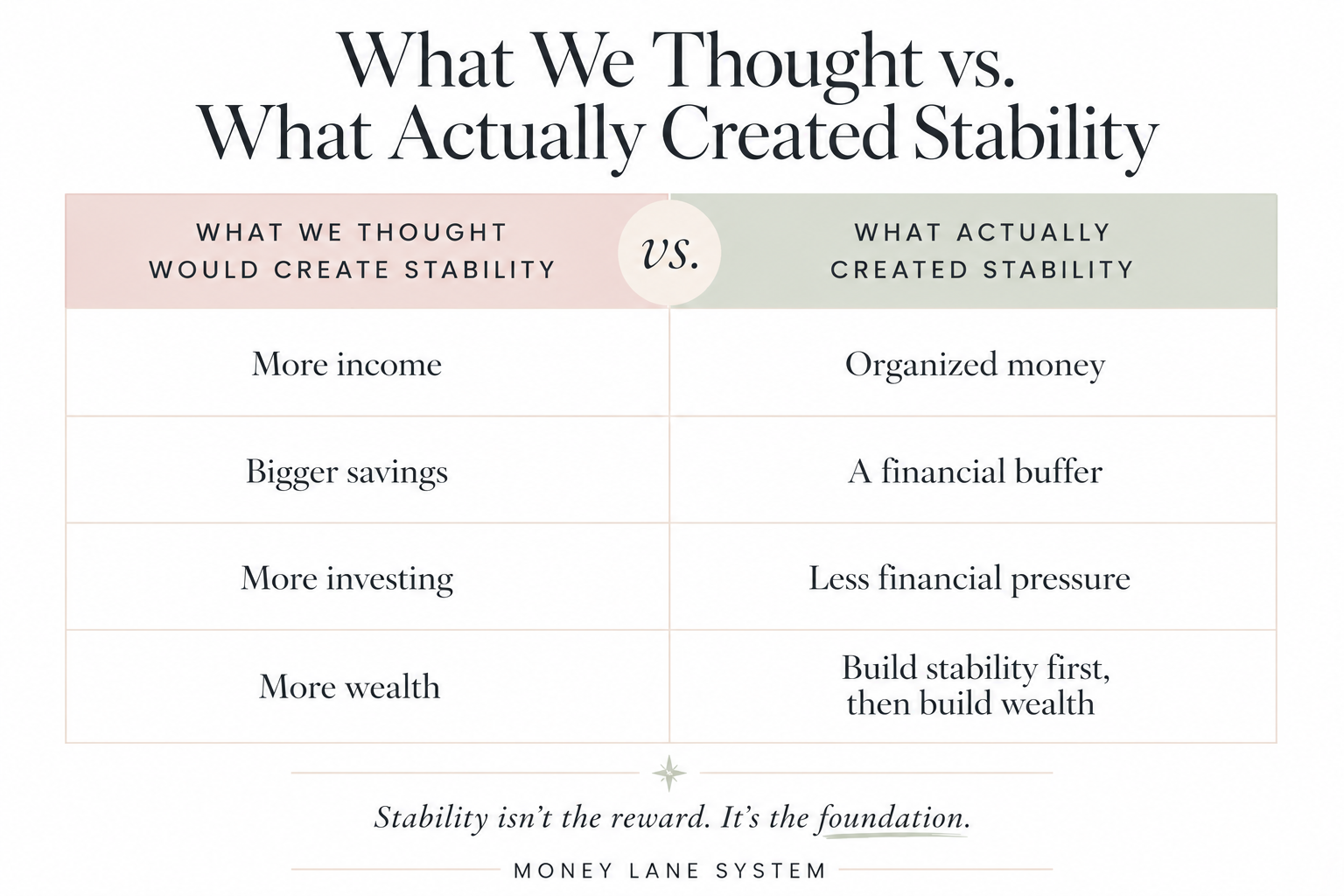

Like many people, we assumed financial stability came after wealth. The plan seemed obvious: make more money, save more money, invest more money, and eventually feel financially secure. What surprised us was discovering the opposite.

The fastest way to build financial stability wasn’t becoming wealthy first. It was creating stability first.

That may sound backwards, but it’s exactly what made it faster. Building wealth often takes years. Sometimes decades. Building stability can start with your next payday.

You don’t need a large investment portfolio to become financially stable. You don’t need to reach financial independence. You don’t need to wait until you’ve accumulated some magical amount of money that finally makes you feel secure. What you need is a plan for the money you already have.

Years later, that realization became the foundation of the Money Lane System.

Before I ever created a financial system, I discovered that financial stability comes from organizing money, preparing for future expenses, and reducing the constant stress that comes from feeling like you’re always one surprise away from falling behind. Once we started doing those things, building wealth became much easier.

For years, we worked hard and did what responsible people are supposed to do. We paid our bills, made our debt payments, and tried to make smart financial decisions. We weren’t constantly in crisis, but we never felt completely comfortable either. There always seemed to be another expense, another setback, or another reason why getting ahead felt harder than it should.

The problem wasn’t that we weren’t trying. The problem was that we were making decisions after money arrived instead of deciding where it needed to go beforehand.

At the time, I thought earning more would solve everything. Maybe if we made a little more money, we’d finally feel secure. Maybe if we saved more, invested more, or reached a certain number in the bank account, the stress would disappear. It never seemed to work that way.

The biggest change wasn’t a raise, an investment, or some complicated financial strategy. The biggest change was getting organized.

We built an emergency fund. We created sinking funds for expenses we knew were coming. We gave every dollar a purpose before it left our account using the same principles that would eventually become the Money Lane System. Instead of constantly reacting, we started preparing.

Looking back, I think this is where a lot of people struggle. They’re trying to build wealth while skipping the things that actually make day-to-day life feel stable. A family with organized finances, a small emergency fund, and a plan for upcoming expenses can sometimes be in a better position than a family earning considerably more but constantly scrambling to keep up.

That’s one reason I think people often rush into investing before they’ve built much stability at home. Investing matters, but we found it was much easier to focus on growing wealth after we had a solid foundation underneath us. That’s why I believe financial stability before investing is a conversation more people should have.

After a few months, we noticed something changing. The stress started fading.

I wasn’t checking the bank account before every grocery trip. Unexpected expenses stopped ruining entire weeks. Conversations about money felt less tense. If you’ve ever dealt with financial stress, you know how exhausting it can be.

For us, the biggest change wasn’t having more money. It was spending less time thinking about money.

Nothing dramatic happened overnight. There wasn’t a huge raise. There wasn’t a windfall. There wasn’t a moment where we suddenly felt rich. What changed was that it finally felt like there was some space between us and the next surprise expense.

For the first time, a vehicle repair, higher utility bill, or unexpected expense didn’t automatically threaten to throw everything off track. Once money felt less chaotic, it became easier to make good decisions. We saved more consistently, planned further ahead, and stopped undoing our progress every time life threw us a curveball.

Looking back, this is the mistake I see people make all the time. They’re focusing on investments, side hustles, and growing their net worth while still dealing with constant money stress.

When every unexpected expense feels urgent, it’s difficult to think beyond the next few weeks. When every paycheck already has too many demands attached to it, it’s difficult to get ahead. That’s why one of the most helpful habits we developed was deciding what each paycheck needed to accomplish before spending started. That simple shift helped us more than any budget ever did.

If you struggle with that, What To Do Every Payday Before Your Money Disappears is a good place to start.

When you’re living paycheck to paycheck, it’s difficult to focus on long-term goals because all of your attention is focused on making it to the next payday. We lived there for years.

And when you’re living paycheck to paycheck, even a fairly ordinary expense can feel enormous because there’s nothing standing between that expense and your next payday. That’s exactly why emergency funds and sinking funds help create stability so quickly. They create a buffer between today’s problems and tomorrow’s paycheck, giving you time and options when life throws something unexpected your way.

In fact, if someone asked me for the fastest way to build financial stability, one of the first things I’d tell them is to focus on How to Save Your First $1,000 Fast. That first $1,000 won’t solve every problem, but it can completely change how it feels when life happens.

We also learned that avoiding common Emergency Fund Mistakes mattered just as much as building the fund in the first place.

Over the years, we knew plenty of people who believed financial security would arrive once they made enough money. Just get the bigger salary. Build the bigger investment account. Keep climbing. Eventually everything would feel settled.

I understand why people think that way. But what I noticed was that some people with good incomes still seemed stressed about money, while other people with much smaller incomes seemed surprisingly comfortable. The difference wasn’t always how much money they made. Often, it was how organized their finances were.

What surprised me was how much better things felt before our income changed very much and before our investments had grown into anything meaningful. Our finances simply became easier to manage.

We worried less, planned better, and stopped feeling like we were constantly trying to catch up.

That’s ultimately why I created the Money Lane System. I wasn’t trying to invent a system. I was just tired of feeling like money needed so much attention all the time.

I didn’t want to spend my evenings updating spreadsheets or tracking all my purchases. I wanted a simple way to know the bills were covered, future expenses were accounted for, and we weren’t constantly being caught off guard.

The Money Lane System came later. It was simply a way of putting a name to the approach that had already transformed our finances. It became our money management system for organizing money before it was spent instead of trying to figure it out afterward.

Looking back, the biggest lesson wasn’t about investing, earning more, or becoming wealthy. It was realizing how different life feels when the next surprise expense doesn’t automatically become a problem.

We spent years thinking more money would make us feel secure. What actually made the difference was having a better plan for the money we already had. Once we figured that out, getting ahead became a whole lot easier.