The first thing I used to do when my paycheck hit my account was pay whichever bill felt the most urgent. Sometimes it was rent. Sometimes the power bill. Sometimes a credit card payment I was already anxious about.

I thought I was being responsible, and honestly, I was trying to be responsible.

But what I didn’t realize at the time was that I was making every money decision from a place of panic instead of stability.

Some nights I would go to bed with my phone volume up so I’d hear the paycheck notification come through. Then I’d wake up and start moving money around before I went back to bed. At the time, that felt normal to me. My paycheck would hit my account, and within minutes I was already trying to stop something from falling behind.

I wasn’t organizing my money. I was reacting to problems one at a time.

Even after bills were paid, I still never trusted what was left in my account. I would check my bank balance before grocery shopping and quietly calculate upcoming bills while pushing a cart around the store. Some mornings I opened my banking app before I even got out of bed because I needed to know what kind of week I was walking into.

Everything felt temporary. Like I was constantly trying to survive until the next paycheck instead of actually getting ahead.

And because all my money sat together in one account, every purchase carried pressure with it. Bill money was mixed with grocery money. Grocery money was mixed with gas money. Future money was mixed with everyday spending. Nothing actually felt safe to spend because every dollar already belonged somewhere else.

That pressure followed me everywhere.

I could be driving to work, folding laundry, or trying to fall asleep while part of my brain quietly calculated bills in the background. I knew exactly which bills had cleared just by looking at my account balance. After a while, I stopped noticing how much space money stress was taking up in my life because it had become normal.

For years, I thought the answer was budgeting harder.

I Needed a Simpler Money Management System

I downloaded apps. Restarted spreadsheets. Tried cash stuffing. Tried spending trackers. Tried strict categories. Every month started with good intentions, and something small always knocked things sideways again. A higher grocery bill. A school expense. A stressful week where convenience spending quietly piled up because I was exhausted.

Every failed budget made me think I lacked discipline.

But after years of repeating the same cycle, it finally became obvious that I did not have a budgeting problem. I had a money organization problem.

I kept trying to manage money better with budgets when the real problem was how my money was flowing once it hit my account. Everything was reactive because nothing had a clear place to go first.

Eventually I stopped trying to build better budgets and started building a better way to organize my money instead. That idea eventually became the foundation for the Money Lane System.

I wrote it because I was tired of financial advice that treated ordinary people like they were careless when most of us are already thinking about money constantly.

Honestly, most people already care too much about money. That’s part of the problem.

The problem usually is not that people do not care. The problem is that their money is being pulled in ten directions before they have a chance to organize it.

If you’ve ever wondered why payday still somehow feels stressful even after getting paid, you’d probably relate to The Hidden Paycheck Trap: Why Payday Still Feels Stressful because that cycle kept repeating for me for years.

Why My Paycheck Never Actually Solved the Problem

The biggest change happened when I stopped asking:

“What should I pay next?”

And started asking:

“What does this paycheck need to cover most?”

That question changed everything.

Instead of paying whichever bill felt the most urgent, I started organizing my money in a specific order. Housing came first. Utilities. Groceries. Transportation. Minimum payments. Then extra debt payments. Then future money.

For the first time, my paycheck had priorities instead of panic attached to it.

Once those essentials were separated first, things started getting quieter. I stopped opening my account wondering whether I forgot something important. Grocery shopping stopped carrying the same level of stress because I already knew the important money was protected.

For the first time in years, I stopped living in constant reaction mode.

It was such a relief not to be so freaking stressed all the time. I had more patience. I was happier. Even my kids noticed the difference.

The article Why Budgeting Fails For Most People (And What Works Better) goes deeper into this because I genuinely believe many people do not need stricter budgets. They need clearer ways to organize their money and fewer daily money decisions.

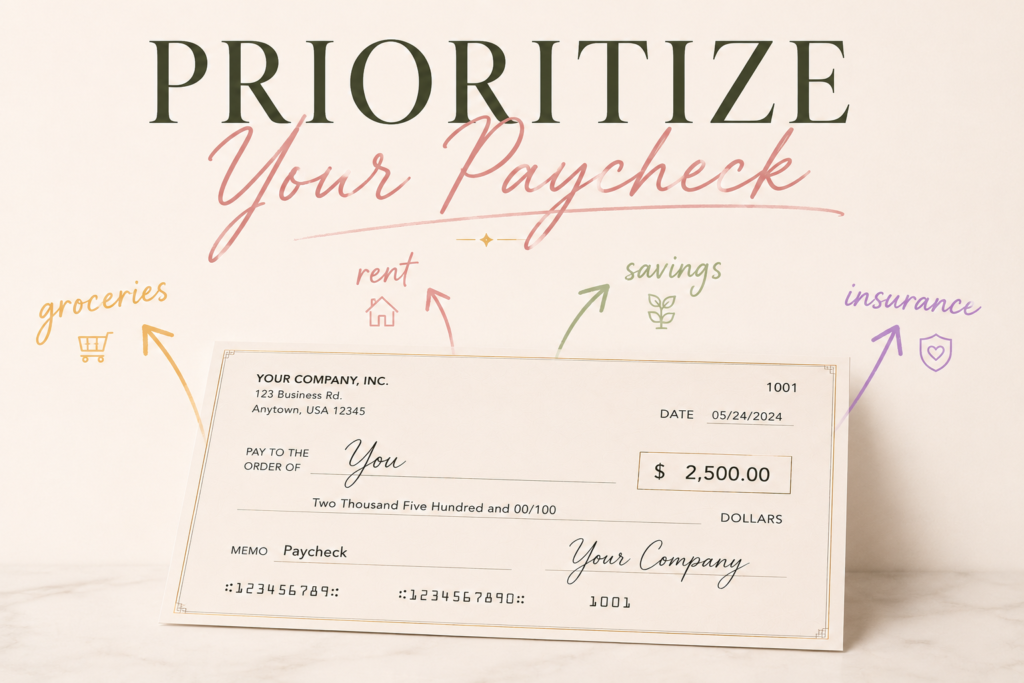

Where My Money Goes First Now

Now when my paycheck comes in, the first thing I do is separate it into three different accounts.

1. Bills and Essentials

This account covers housing, utilities, groceries, transportation, insurance, and the things that keep life functioning normally.

2. Everyday Spending

This is the money I can actually use without accidentally spending grocery money, rent money, or bill money without realizing it.

3. Future Money

This account is for savings, emergency money, bigger upcoming expenses, and the money that slowly stops life from constantly feeling like everything might fall apart.

Most of it happens automatically now.

And maybe the biggest difference is that I’m no longer lying in bed at 1:30 in the morning moving money around trying to prevent some kind of disaster before I go back to sleep.

My paycheck already has direction before everyday life starts taking pieces of it.

If you’re trying to organize your money better without constantly tracking every dollar, The Best Bank Account Setup for Managing Money Without Budgeting explains the exact setup that helped me stop mixing all my money together.

Organizing My Money Changed My Spending Too

One thing that surprised me was how much my spending changed once my money became organized.

Before, I thought I had an impulse spending problem. But honestly, a lot of my spending came from exhaustion. Ordering takeout after hard days. Buying small things because life already felt stressful. Spending for temporary relief because my finances constantly felt chaotic anyway.

Once my essentials were protected first, a lot of that started calming down naturally.

Not perfectly. But noticeably.

I also stopped thinking about money every hour of the day. Before, my brain was always running calculations in the background:

- what bills were still coming out,

- whether there was enough for groceries,

- whether I forgot something automatic,

- whether one unexpected expense was about to ruin the month.

That kind of pressure wears you down slowly.

Separating my money changed that.

And honestly, it changed my money management more than any budget spreadsheet or finance app ever did.

If you struggle with overspending because your finances constantly feel chaotic, How to Control Your Spending Without Tracking Every Dollar explains this in more detail.

You might also relate to Digital Envelope Budgeting Explained (The Easy Way to Manage Money) if you’ve tried cash stuffing or envelope systems but still found yourself constantly moving money around between categories.

I’m Not Rich Now, But I’m Stable

And honestly, that’s what I wanted the entire time.

Bills get paid. Groceries are normal again. One unexpected expense no longer destroys my entire month. I no longer wake up already anxious about my bank account before my feet even hit the floor.

I spent years thinking stability would come from making fewer mistakes. What actually changed my life was giving my money direction before the month had a chance to take it from me.

If you’re exhausted from living paycheck to paycheck, this is where I would start: stop waiting to see what survives at the end of the month. Decide where your money needs to go first.

That single change did more for my finances than years of budgeting ever did.