I was 12 years old when I got my first bank card.

I remember promising my mom and dad that I’d be responsible with money. I was going to budget carefully, track everything, and spend wisely.

And honestly, it worked.

My 12-year-old financial life was pretty manageable. Lip gloss. Music CDs. Maybe a hoodie from the mall if I saved enough babysitting money. I could track every dollar because there were barely any dollars to track.

What I could never have imagined were the completely ruthless financial hits that show up in adult life.

A transmission replacement that wipes out your savings. A cracked foundation you can’t ignore. A septic tank replacement nobody warns you about until it happens to you. Losing your job because of chronic illness and the prescription and therapy bills that go along with that. Groceries somehow costing almost double what they did only three years ago. One appliance dying right after another like your house has developed a personal vendetta against your bank account.

Nobody explains this part when you’re younger.

Nobody explains how adult money can feel less like “budgeting” and more like trying to survive repeated financial ambushes while still answering emails, making dinner, showing up for work, and pretending you are not quietly panicking inside.

That’s also why tracking every dollar eventually stopped working for me.

My financial life had become too complicated for constant micromanaging. I didn’t need more budgeting categories. I needed less chaos. I needed clearer separation between bills, spending, and future money so everything stopped competing with everything else all the time.

That idea eventually became the foundation for the Money Lane System, which is built around organizing money before it disappears instead of trying to clean up the damage afterward.

And honestly, that changed more than my spending habits.

It changed my stress levels too.

Because somewhere along the way, budgeting had stopped feeling organized and started feeling like constant damage control. You stop tracking little purchases and start mentally carrying unfinished financial thoughts around all day. Did that automatic payment already come out? Is the property tax bill due this week or next week? Can you buy groceries right now or are you forgetting something important? If the car breaks down again, are you completely screwed until payday?

Tracking every dollar feels very different once adult life gets financially complicated.

Adult money is not just math anymore. It’s pressure. It’s unpredictability. It’s waking up at 3 a.m. mentally calculating bills instead of sleeping.

And if budgeting feels exhausting now, it’s probably because your financial life got more complicated while the advice stayed weirdly simplistic.

Why Tracking Every Dollar Can Start Making You Feel Worse

I tried all of it.

Budget apps that sent guilt-inducing notifications. Cash envelopes that worked great until real life stopped cooperating. Spreadsheets that made me feel organized for about four days before I fell behind again. I even tried a no-spend month once, which lasted exactly five days until family showed up unexpectedly from out of town and I suddenly had restaurant bills, extra groceries, and entertainment expenses I never planned for.

Then there were the fresh starts every January where I convinced myself this was finally the year I would become one of those people who color-coded everything and never felt stressed standing in checkout lines.

For a few days, budgeting always felt hopeful.

Then reality would hit again.

I’d need new tires unexpectedly. The dog would need medication. School expenses would appear out of nowhere. I’d have an emotionally exhausting week and order takeout three nights in a row because I genuinely could not handle cooking after spending the entire day trying to hold my life together.

Then the budget would feel ruined, and once it felt ruined, I wouldn’t want to look at it anymore.

If you have ever stopped checking your banking app because seeing the balance made your stomach drop immediately, you already know this cycle.

After a while, it starts feeling like money needs your attention every hour of the day. Constant categorizing. Constant remembering. Constant self-control. When your brain already feels overloaded from everyday life, budgeting starts feeling like one more thing you are failing to keep up with.

That doesn’t mean you are irresponsible.

Your brain is overloaded from trying to manage financial pressure nonstop.

The Real Problem Usually Isn’t Overspending

For years, I thought my biggest issue was overspending.

Sometimes it was.

But more often, the real problem was that all my money lived together in one giant pile.

Bills mixed with grocery money. Emergency savings mixed with spending money. Subscription payments mixed with money I actually needed for next week. Everything sat in the same account together, forcing me to mentally calculate my entire financial life every time I bought anything.

That constant uncertainty creates anxiety fast.

If you regularly check your account before buying groceries or mentally subtract upcoming bills every time you look at your balance, you are not really “tracking spending” anymore. You are trying to survive financial uncertainty in real time while carrying your finances around in your head all day long.

And carrying your finances around in your head all day gets exhausting fast.

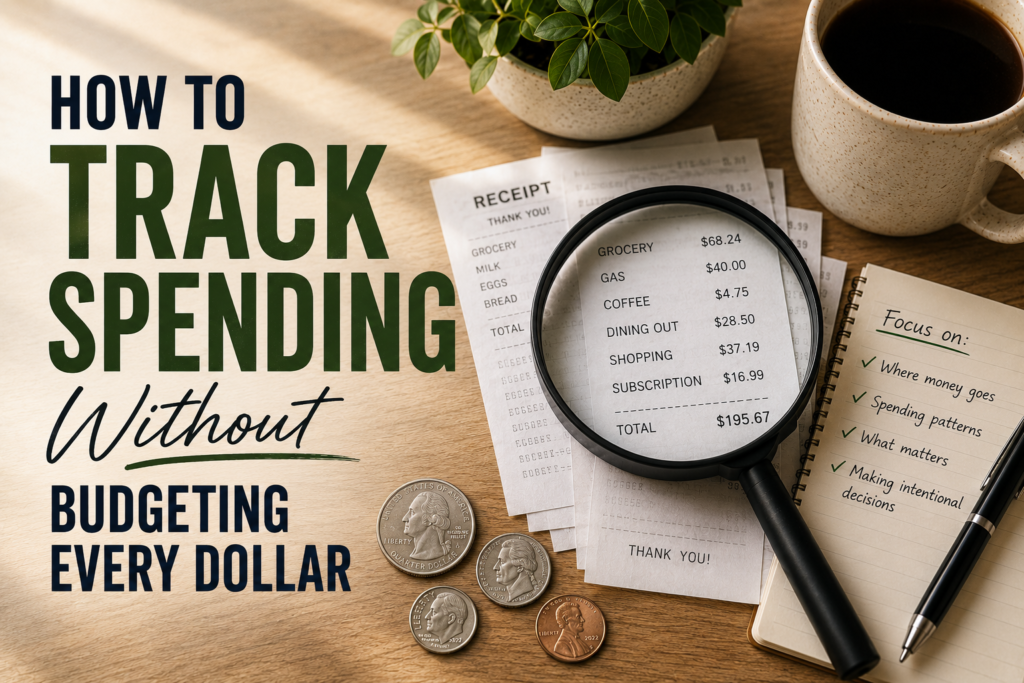

How to Track Spending Without Budgeting Every Dollar

The biggest change for me happened when I stopped trying to monitor every transaction and started organizing my money before I spent it.

No obsessively tracking every coffee purchase. No complicated spreadsheet categories. No trying to remember whether paper towels counted as groceries, household expenses, or some completely different category I’d forget about two days later anyway.

I started separating money into clearer purposes instead.

This is basically how my Money Lane System works.

Your bills lane handles fixed expenses and recurring payments. Your spending lane handles groceries, gas, coffee, takeout, and everyday life. Then your future lane protects money meant for savings, debt payoff, emergencies, and long-term financial goals before it gets absorbed into random spending.

Bills in one place. Spending money in another. Future money somewhere protected from everyday life.

That separation immediately lowered my stress, but the bigger changes came later.

I finally started paying down debt instead of endlessly recycling it. I built an emergency fund that could actually absorb real-life problems. Raises stopped disappearing instantly because every extra dollar finally had direction instead of leaking away into random spending and survival mode.

It also completely changed what financial freedom meant to me.

Not luxury-car freedom. Not influencer freedom.

Just normal-person freedom.

The kind where your car breaks down and you can handle it without spiraling. The kind where payday stops feeling like a temporary rescue mission. The kind where you can finally take a vacation using money you already saved instead of putting the whole trip on a credit card and stressing about it afterward.

The kind where your finances stop taking up so much space in your brain all the time.

That felt bigger than budgeting ever did.

That’s also why posts like How to Organize Your Finances Without a Budget Spreadsheet and The Best Bank Account Setup for Managing Money Without Budgeting connect so strongly with people who feel burned out by traditional budgeting advice. They focus less on micromanaging spending and more on helping you stop feeling financially overwhelmed all the time.

The Spending Account Was More Helpful Than Any Budget Category

One of the simplest changes you can make is creating a separate account just for everyday spending.

Not bills. Not emergency savings. Not future goals.

Just regular life.

Groceries, gas, coffee, random Walmart trips, school lunches, takeout nights when your brain feels fried, and all the little purchases that happen during normal adult life.

That one change removes an unbelievable amount of mental clutter because you stop checking one giant account and trying to remember what still needs to come out of it.

Instead, you only need to know one thing:

How much is left in the spending account?

That becomes your spending tracker automatically.

If the account starts getting low, you naturally slow down. If there’s still room left, you stop panicking over every small purchase. You stop manually tracking dozens of tiny transactions while already emotionally drained from life.

And honestly, clarity feels very different from restriction.

Stress Spending Usually Starts With Exhaustion

Stress spending usually shows up when your brain is exhausted and you just want one thing in life to feel easy for five minutes.

That’s why online shopping gets dangerous late at night. That’s why takeout spending spikes after emotionally exhausting weeks. That’s why impulse purchases suddenly look reasonable after a brutal day where everything felt difficult.

And if your finances already feel unstable, those purchases carry even more emotional weight afterward. You feel guilty immediately. Then anxious. Then avoidant. Then you stop checking your account altogether because the balance feels like one more thing your brain cannot handle.

If this cycle feels familiar, stricter budgeting probably is not the answer.

You probably need less mental clutter around money.

More Budget Categories Probably Won’t Make Your Finances Feel Calmer

You can track tiny purchases perfectly and still feel stressed every payday.

That’s the part budgeting apps rarely fix.

Simpler setups are easier to stick with because your brain stops managing money every waking minute. Clearer separation creates calmer decisions because you stop mentally juggling your entire financial life every second of the day.

If detailed budgeting has never felt sustainable for you, read Why Budgeting Fails for Most People (And What Works Better) too.

You do not need financial perfection.

You need your money to stop feeling like a constant source of pressure.

The Real Goal Is Feeling Less Financially Overwhelmed

If you ended up here after searching for ways to stop overspending, simplify budgeting, or finally feel more in control of your money, you probably are not looking for another spreadsheet.

You are looking for relief.

You want grocery shopping to feel normal again instead of stressful. You want payday to stop feeling like a temporary reset button. You want to open your banking app without immediately wondering what went wrong this time.

More than anything, you want to stop feeling like one unexpected expense could derail your entire month emotionally and financially.

That kind of stability improves your quality of life far more than perfectly organized budget categories ever will.

If You’re Tired of Restarting Budgets Over and Over

You are probably not failing because you “lack discipline.”

You are probably exhausted from trying to manage adult financial pressure with systems that require constant attention and emotional energy.

A calmer financial setup works differently. It reduces the number of decisions you have to make every day. It creates clearer boundaries around spending. It protects important money before life gets a chance to consume it.

That’s why the Money Lane System focuses so heavily on separating bills, spending, and future money ahead of time instead of obsessively tracking purchases afterward.

And honestly, the biggest change for me was not becoming “better” with money. It was finally feeling less panicked around it. Because when your finances stop feeling chaotic, your entire life feels lighter too.

Not perfect.

Just lighter.